One of the most misunderstood parts of buying a home is mortgage insurance.

Many buyers in Monroe County, including Stroudsburg and Tannersville, are surprised when they discover that their monthly payment includes an additional insurance charge that does not protect them—it protects the lender.

Understanding how mortgage insurance works can save you thousands of dollars and help you make smarter financing decisions.

Let’s break it down clearly.

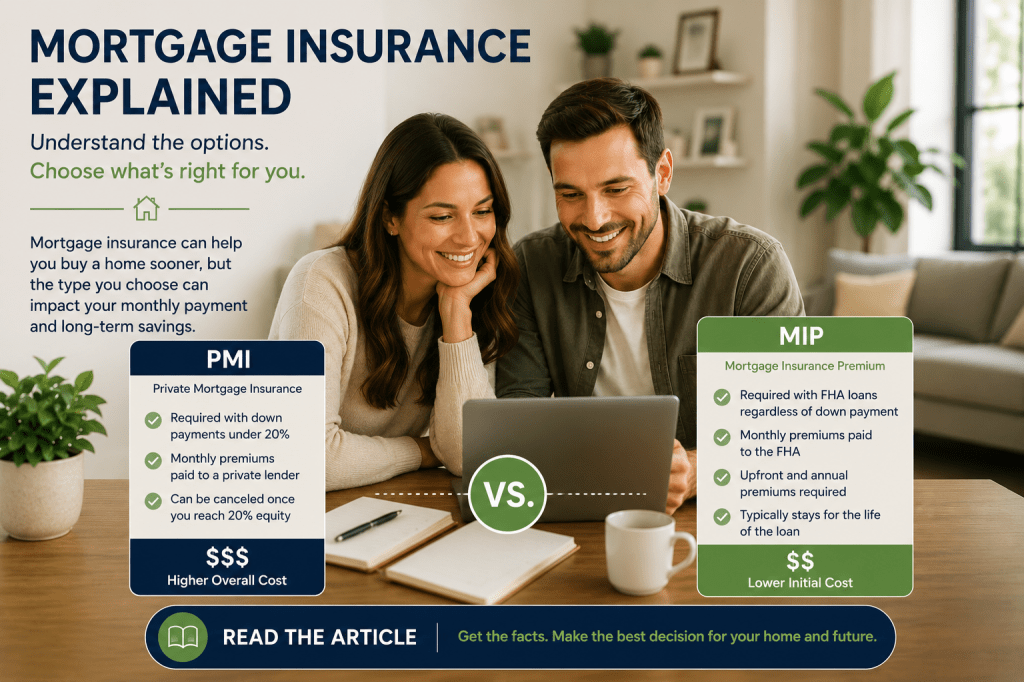

What Is Mortgage Insurance?

Mortgage insurance is a policy that protects the lender if the borrower stops making payments and defaults on the loan.

There are two primary types:

- PMI (Private Mortgage Insurance) → Typically associated with conventional loans

- MIP (Mortgage Insurance Premium) → Associated with FHA loans

While both serve a similar purpose, they operate very differently.

What Is PMI (Private Mortgage Insurance)?

PMI is generally required on a conventional loan when the buyer puts down less than 20%.

For example:

- Purchase Price: $400,000

- Down Payment: 5% ($20,000)

- Loan Amount: $380,000

Because the lender considers this a higher-risk loan, PMI is added.

How Much Does PMI Cost?

PMI costs vary depending on:

- Credit score

- Down payment amount

- Loan type

- Debt-to-income ratio

- Loan size

In most cases, PMI ranges from:

- 0.3% to 1.5% of the loan amount annually

Example:

A borrower with a $350,000 loan may pay:

- Approximately $100–$400 per month in PMI

Buyers with:

- Higher credit scores

- Larger down payments

- Lower debt levels

typically receive lower PMI costs.

Can PMI Be Removed?

Yes—and this is one of the major advantages of conventional financing.

Under federal law, PMI on most conventional loans must:

- Automatically terminate once the loan reaches 78% loan-to-value (LTV) based on the original purchase price

- Be removable by request at 80% LTV

In practical terms, this means:

- Once you build enough equity, you may no longer need PMI

How Do You Remove PMI Faster?

There are several strategies:

1. Pay Down the Mortgage Faster

Making additional principal payments accelerates equity growth.

Even one extra payment per year can shorten the timeline.

2. Increase Property Value

If home values rise significantly in Monroe County or you improve the property through renovations, you may qualify for PMI removal sooner.

Lenders often require:

- A new appraisal

- Proof of payment history

- Sufficient equity

This can be particularly valuable in appreciating markets like parts of the Pocono region.

3. Refinance the Loan

Some homeowners refinance into a new conventional loan after building equity.

If the new loan balance is below 80% of the home’s value, PMI may disappear entirely.

However, refinancing only makes sense if:

- Interest rates are favorable

- Closing costs justify the savings

- Long-term payment structure improves

What Is MIP (Mortgage Insurance Premium)?

MIP is the mortgage insurance attached to FHA loans.

Unlike PMI, FHA mortgage insurance consists of two separate costs:

1. Upfront Mortgage Insurance Premium (UFMIP)

Typically:

- 1.75% of the loan amount

This amount is often rolled into the mortgage rather than paid out of pocket.

2. Annual Mortgage Insurance Premium

This is paid monthly as part of the mortgage payment.

The amount varies based on:

- Down payment

- Loan term

- Loan amount

For many FHA borrowers, this adds:

- Approximately 0.45%–1.05% annually

Can You Remove FHA MIP?

This is where many buyers become frustrated.

For many FHA loans:

- MIP does not automatically disappear

The rules depend on your down payment.

If You Put Less Than 10% Down:

MIP typically remains for the life of the loan.

If You Put 10% or More Down:

MIP is generally removed after 11 years.

How Do Homeowners Get Rid of FHA MIP?

The most common solution is refinancing into a conventional loan once sufficient equity exists.

Homeowners often refinance when:

- Their credit improves

- Home values increase

- They reach at least 20% equity

This can eliminate mortgage insurance entirely.

Which Is Better: PMI or MIP?

The answer depends on your financial profile and goals.

Conventional Loans with PMI Often Benefit:

- Buyers with stronger credit

- Buyers planning long-term ownership

- Buyers expecting equity growth

FHA Loans Often Benefit:

- First-time buyers

- Buyers with lower credit scores

- Buyers with smaller down payments

In some cases, FHA financing can be the best entry point into homeownership—even with MIP.

The key is understanding the long-term cost structure before committing.

Final Thoughts for Buyers in Monroe County

Mortgage insurance is not necessarily “bad.” In many cases, it allows buyers to purchase a home sooner rather than waiting years to save 20% down.

However, buyers should understand:

- What they are paying

- Why they are paying it

- How long it may remain

- The strategy for eventually removing it

A smart home purchase is not just about qualifying for the loan—it is about understanding the full financial picture.

Thinking About Buying a Home in Stroudsburg, Tannersville, or Monroe County?

If you are planning to buy a home and want clear guidance on:

- Loan options

- Down payment strategies

- Monthly payment structure

- Conventional vs. FHA financing

- Long-term equity planning

I’d be happy to help you navigate the process strategically.

Reach out today for a buyer consultation and personalized guidance tailored to your goals and budget.

The right financing strategy can save you thousands over the life of your loan.